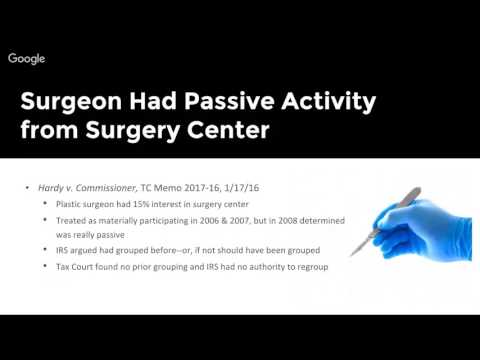

This is the current federal tax development for the week of January 23rd, 2017. Current federal tax developments are brought to you by your state Society of CPAs and Nichols Patrick CPE, a division of Valois Causal Institute. This week we will look at the following developments: - A discussion on a release granted by the IRS when a CPA firm failed to have a client file a Form 3115. - The IRS loses a case on a passive activity issue when the Tax Court accepts the logic of a technical advice memorandum issued by the IRS after the trial concluded. - The tax court applies the Rank Meyer case decision against the IRS in a second issue on the same case. - The IRS would not allow an employer to voluntarily pay money after the statute of limitations had closed due to an error in the payroll tax report. - A preview of the proposed regulations issued by the IRS dealing with the comprehensive partnership audit rules. We will discuss some of the highlights of the proposed regulations but will do a deeper dive in the coming weeks due to the length of the document. In addition to these developments, there are four upcoming federal tax update sessions for CPAs and industry professionals in Ohio. The sessions will be held on February 14th, 16th, 17th, and 24th in Cincinnati, Fairfield, Toledo, and Columbus, respectively. The sessions will also be webcasted by the Ohio Society of CPAs. Now, let's move on to the first issue discussed in this update. Private Letter Ruling 2017-21 was issued on January 13th and addresses the change in method of accounting for prepaid insurance. The taxpayer, in consultation with their CPA, decided to change their method of accounting to accelerate their deduction for insurance. However, due to various complications within the CPA firm,...

Award-winning PDF software

Video instructions and help with filling out and completing Will Form 843 Tangible