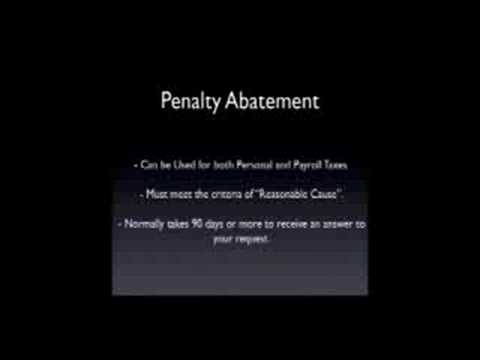

IRS penalty abatement is a potential solution in most cases of IRS problem resolution, except when the case is being resolved through full payment, bankruptcy, or an accepted offer and compromise. If you are entering into an installment agreement or facing financial hardship, it may be advisable to request penalty abatement. Both personal and payroll taxes can be subject to penalties, but they can be abated if the taxpayer can demonstrate reasonable cause. Reasonable cause means that despite exercising ordinary care, unforeseen circumstances led to the failure to file or pay taxes on time. Providing a reasonable explanation is crucial, particularly couching it in terms of ordinary business care and prudence. For instance, if a hurricane caused the loss of business records, it can be a valid reasonable cause. However, the longer the duration of non-compliance, the harder it becomes to achieve penalty abatement. The IRS may respond to a request within 90 to 180 days, sometimes requesting full payment before considering the abatement. However, this requirement is not supported by the law. If faced with this response, it is possible to write a letter asserting the incorrectness of the demand. The request should be sent via certified mail with a return receipt requested, and attention should be given to addressing it to the penalty abatement coordinator. Sending a request without certified mail increases the chances of it being disregarded. If dealing directly with a revenue officer, the request should be directed to them, with clear emphasis on the request for penalty abatement. It is important to avoid incorporating too many topics in the letter to prevent rejection by the revenue officer.

Award-winning PDF software

Video instructions and help with filling out and completing Form 843 Penalties